- An investment manager can use the slope and inflection of a target-date glide path to address specific risks of plan participants

- Mitigating the risks that a glide path is best suited to address calls for a steeper slope than the current industry average

- For glide path design, investment managers should identify the most representative assumptions for the participant population

In our previous commentary, we explained that a target-date glide path cannot address all risks faced by retirement savers, and that the most important consideration for investment managers is sequence-of-returns (or sequence) risk. In this commentary, we will share our view on determining the overall shape of the glide path.

How a glide path helps manage sequence risk

Sequence risk will have an effect on all participants who depend on their portfolio for retirement income. Every traditional glide path that decreases equity over time is subject to sequence risk; however, where on the glide path a participant is most vulnerable — and where there is any resulting tradeoff — depends on how the investment manager chooses to address sequence risk.

The best approach to designing a glide path to address sequence risk, we believe, requires an initial focus on the sensitivities of portfolio size, investor time horizon, and portfolio volatility. These factors are the reasons why sequence risk is greatest near and during retirement, and indicate that a risk parity portfolio allocation is most appropriate at these later stages of the glide path.

Looking at the early stages

One could logically propose that a glide path should start out as aggressive as possible, given that the portfolio balance/contributions are typically lower and the time horizon is long. It should then transition to become much more conservative around and in the retirement phase. This would necessitate a glide path that appears much steeper than the current industry average.

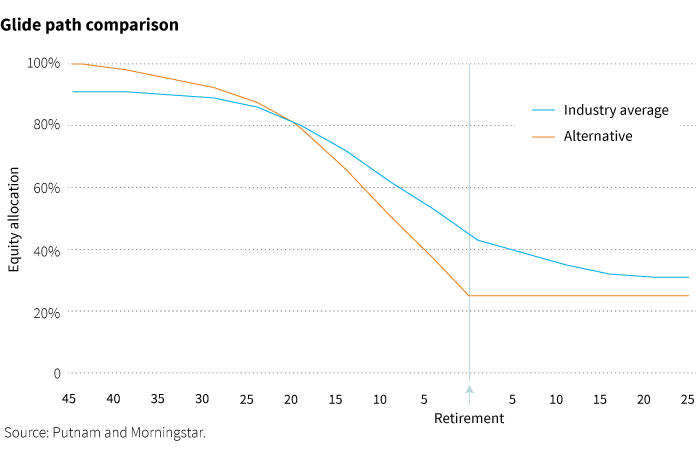

Determining the inflection point

The steepest part of the slope for this alternative glide path is where it is most vulnerable to sequence risk. Philosophically, it seems sensible that a portfolio would be most sensitive to sequence risk at a stage when a participant still has many levers to control in response. In the alternative glide path, this stress point is when the participant still has around 15 years to retirement. In the event of an adverse market event at this point, the participant has many other options to implement (e.g., increase savings, delay retirement), and can hopefully recover from the setback.

Adjustments in the distributions phase

In contrast, for glide paths that are more aggressive and/or continue to reduce equities in the distributions phase, the timing of this stress point often comes after retirement. Should an adverse market event occur after retirement, the ability of individuals to adjust their situation is much more limited.

A shallower path misaligns risks

In another approach, managers may choose to deal with sequence risk by minimizing the size and/or frequency of portfolio reallocations, resulting in a much shallower, flatter shape to the retirement glide path. Conceptually this approach should minimize sequence risk at any point in time; however, it likely overemphasizes sequence risk early on at the expense of shortfall risk, failing to take advantage of the longer time horizon before withdrawals, while being too aggressive toward the maturity date, exposing the participant to much more volatility than needed.

Focus on participant needs

It is impossible to say a glide path is optimal, even under a certain set of assumptions. Instead, managers must first identify the most representative set of assumptions for the participant population, and then make hard decisions around the costs and benefits of managing the numerous risks facing participants at various points along the glide path.

Of all the risks retirement plan participants face, sequence risk should be of the utmost concern to an investment manager, as this risk will impact those plan participants who will depend on their portfolio for retirement income. Avoiding a significant drawdown to the retirement portfolio near the retirement date is paramount. When these losses occur in close proximity to retirement, they have the potential to impair the retirement portfolio to such an extent that it may no longer be able to meet the needs of the plan participant throughout retirement.

Read more about our views on target-due fund considerations in "The glide path less traveled."

Consider these risks before investing: Our allocation of assets among permitted asset categories may hurt performance. Stock and bond prices may fall or fail to rise over time for several reasons, including general financial market conditions, changing market perceptions (including, in the case of bonds, perceptions about the risk of default and expectations about monetary policy or interest rates), changes in government intervention in the financial markets, and factors related to a specific issuer or industry. These and other factors may lead to increased volatility and reduced liquidity in the funds’ portfolio holdings. Growth stocks may be more susceptible to earnings disappointments, and value stocks may fail to rebound. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk (the risk of bond prices falling if interest rates rise) and credit risk (the risk of an issuer defaulting on interest or principal payments). Default risk is generally higher for non-qualified mortgages. Interest-rate risk is greater for longer-term bonds, and credit risk is greater for below-investment-grade bonds. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk and the risk that they may increase in value less when interest rates decline and decline in value more when interest rates rise. International investing involves currency, economic, and political risks. Emerging-market securities carry illiquidity and volatility risks. Active trading strategies may lose money or not earn a return sufficient to cover trading and other costs. REITs are subject to the risk of economic downturns that have an adverse impact on real estate markets. Commodity-linked notes are subject to the same risks as commodities, such as weather, disease, political, tax and other regulatory developments, and other factors affecting the value of commodities. Risks associated with derivatives include increased investment exposure (which may be considered leverage) and, in the case of over-the-counter instruments, the potential inability to terminate or sell derivatives positions and the potential failure of the other party to the instrument to meet its obligations. Efforts to produce lower volatility returns may not be successful and may make it more difficult at times for the funds to achieve their targeted returns. In addition, under certain market conditions, the funds may accept greater volatility than would typically be the case, in order to seek their targeted returns. There is no guarantee that the funds will provide adequate income at and through an investor's

retirement. You can lose money by investing in the funds.

For the portion invested in Putnam Government Money Market Fund, these risks also apply: You can lose money by investing in the fund. Although the fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. The fund may impose a fee upon the sale of your shares or may temporarily suspend your ability to sell shares if the fund’s liquidity falls below certain required minimums because of market conditions or other factors. An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The fund’s sponsor has no legal obligation to provide financial support to the fund, and you should not expect that the sponsor will provide financial support to the fund at any time.

The values of money market investments usually rise and fall in response to changes in interest rates. Interest-rate risk is generally lowest for investments with short maturities (a significant part of the fund’s investments). Although the fund only buys high-quality investments, investments backed by a letter of credit have the risk that the provider of the letter of credit will not be able to fulfill its obligations to the issuer. The effects of inflation may erode the value of your investment over time.

The principal value of the fund is not guaranteed at any time, including at the target date.

312579

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.