- Average DC plan total savings rates continue to rise, standing at 13.2% as of 2018.

- The current industry average glide path is likely too aggressive given the higher savings rates.

- The goal of a glide path should be to provide adequate income throughout retirement with more predicable outcomes.

A recent study conducted by Fidelity Investments highlighted recent trends and insights across the retirement landscape (“Building Financial Futures: Trends and insights of those saving for retirement across America.”). The data analyzed by Fidelity, as of March 31, 2018, focuses on approximately 22,600 corporate DC plans and 15.8 million participants. Fidelity found that average DC plan total savings rates (i.e., employee + employer contributions combined) have increased to 13.2% in 2018, from 12.7% in 2016, an encouraging statistic. This is a significant development, and asset managers responsible for managing target-date-funds (TDFs) should carefully incorporate this information and how it affects the resulting equity allocation across the glide path.

The impact of savings rates

There are many factors that influence the probability of success for plan participants, but none affects outcomes quite like the savings rate. The importance of savings rates has been well documented by retirement industry leaders. Putnam’s research, summarized in our April 2018 paper, The glide path less traveled, suggests that in order to maintain the same success probability, every 1% decrease in the savings rate necessitates a 10% increase in the equity allocation throughout the entire glide path. Typically, this sobering fact is often used to explain why, for plan participants who save too little, there is no amount of equity allocation that can consistently make up that deficiency. Instead of relying on savings, success will effectively be dependent upon a fortunate series of market returns, akin to a lottery ticket approach. It should be no surprise then that a large component of plan design and participant education focuses on increasing plan savings rates. Fidelity’s data suggest these efforts are having a positive effect.

The implication for target-date fund allocations

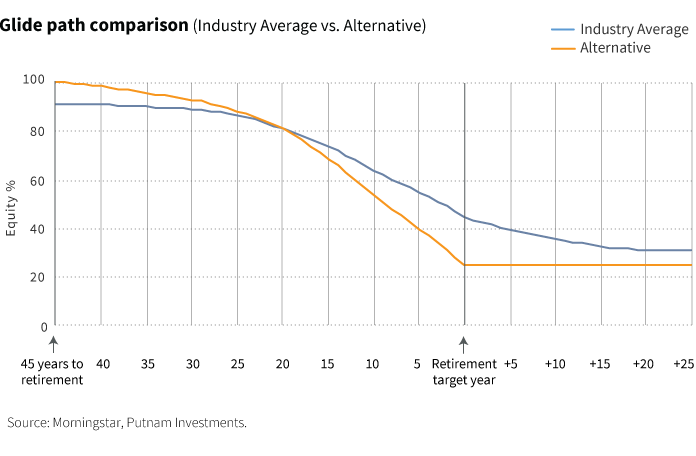

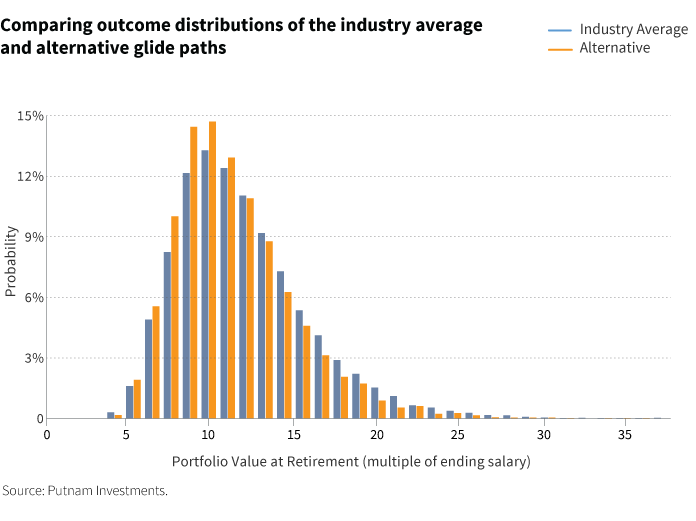

What does this mean for TDF managers in how they allocate to equities across the glide path? If lower savings rates necessitate increases in the equity allocation throughout the glide path, then it is reasonable to suggest that higher savings rates should result in a reduction in equity across the glide path. Even today, using a fairly conservative 10% combined savings rate, Putnam’s analysis suggests that the industry average glide path may be too aggressive for the median plan participant (see chart 1), and that an alternative glide path — one that is slightly more aggressive early on, but much more conservative as one approaches retirement — can lead to more consistent outcomes (see chart 2).

Sustaining savings versus maximizing wealth

An obvious counterargument is that higher savings rates will lead to more fully funded retirement accounts, which in turn, have the ability to bear more risk. That textbook logic is sound if one is purely seeking to maximize ending wealth; however, in our opinion, that should not be the baseline assumption for a TDF manager. The main goal of a TDF should be to provide adequate wealth throughout retirement. In that scenario, retirement success is defined as a participant reaching life expectancy with a non-zero portfolio balance, not maximizing ending wealth. For the greatest likelihood of achieving that goal when designing a glide path, a manager should focus on the central tendency of a given assumption, and then appropriately weigh the costs and benefits of managing the numerous risks facing participants.

The consequence of higher savings

Providing broad access to workplace savings is necessary to begin to solve today’s retirement challenges. Once a participant is enrolled in a plan, increasing his/her savings rate is paramount. If recent savings trends as documented in the Fidelity study persist, it is welcome news; however, it will also necessitate changes in how a TDF manager allocates to equities across the glide path to create successful, predictable outcomes for their participants. For more reasons why this is so, read Putnam's The glide path less traveled.

313988

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.