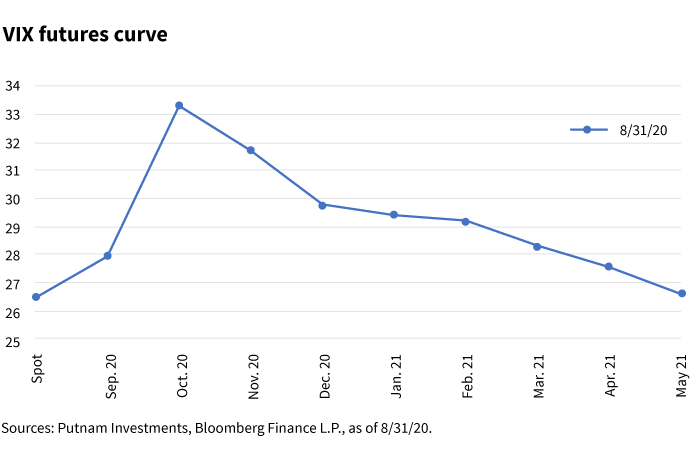

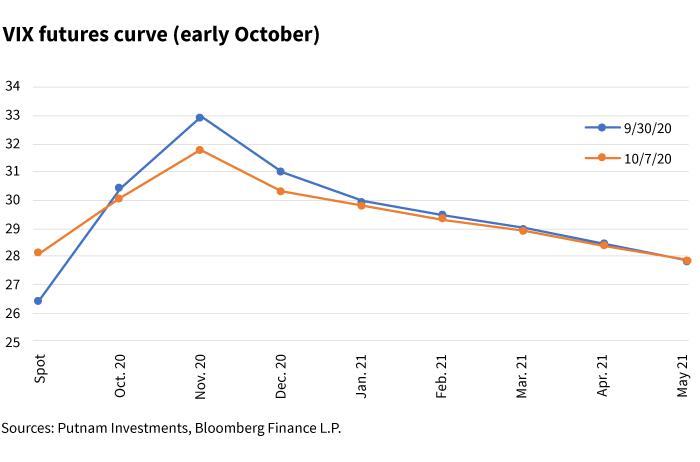

In “normal” markets, the VIX futures curve historically has an upward slope, and it inverts during risk-off episodes (VIX is the CBOE Volatility Index, and it is a measure of expected volatility in the next 30 days). However, when there are well-known catalysts (e.g., elections, Federal Reserve meetings), the curve can experience a “kink” to price in that idiosyncratic risk. Below is the VIX futures curve from the end of August 2020:

Note that a VIX futures contract converges to the value of the VIX on the day the contract expires. In this case, the October VIX future contract, which expires on October 21, will converge to the value of VIX on that date. The price of the VIX on October 21 is itself an expectation of the volatility in the thirty days from October 21 to November 20. Since that period includes Election Day (November 3), the kink in the curve is in October.

Probability of delayed election result

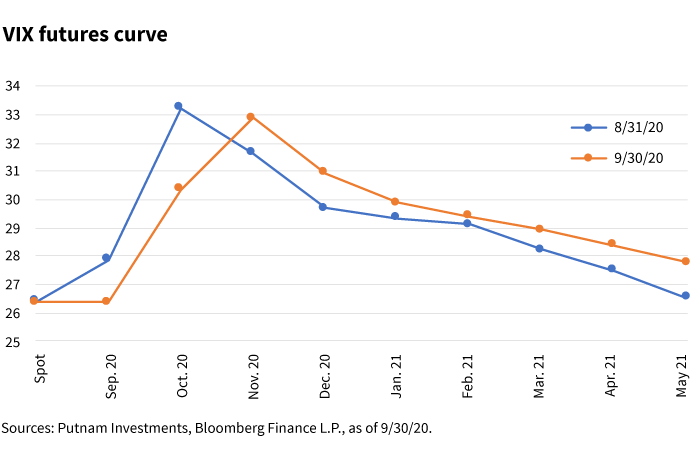

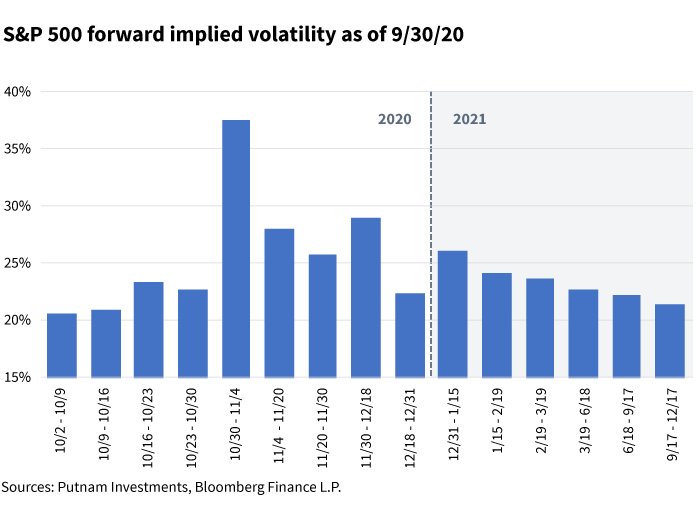

However, with growing uncertainty around the actual election (counting ballots amid the COVID-19 pandemic), the declaration of a winner (the possibility of a court challenge as in 2000) and a potential messy transfer of power (President Trump has made statements that he would not accept the election results), the volatility markets are starting to price these risks further into the future, rather than on Election Day. Below are the VIX futures curves as of August 31 and September 30.

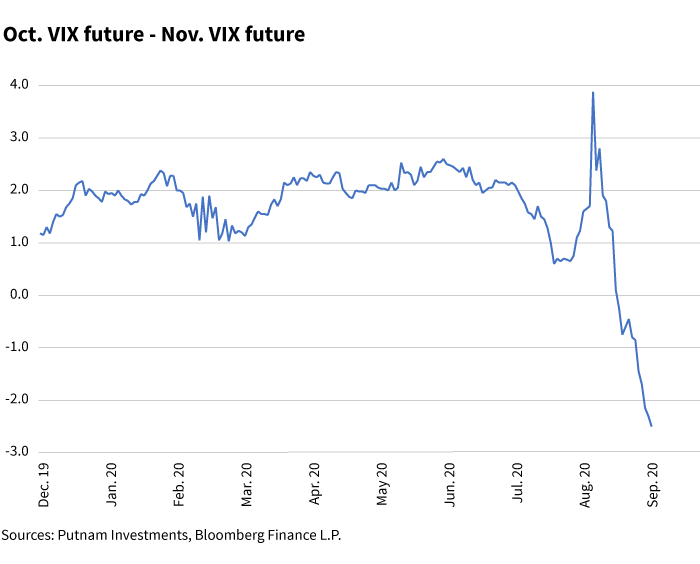

Notice that the kink has now moved to the November futures contract (election aftermath), with even the December future priced higher than the October future. This was a result of the October future falling significantly while the November and December (and even January) futures all moving higher. This shifting of the kink from October to November is a recent phenomenon:

[caption width="700" align="alignnone"] October VIX futures[/caption]

October VIX futures[/caption]

This means volatility markets are now pricing in a large likelihood of drawn-out election uncertainty, possibly all the way up to inauguration day. However, the movement of the kink from the October future to the November future does not mean that markets are expecting the aftermath to be riskier than the election itself. One subtlety lost in the VIX futures curve being monthly is that the market is pricing in a big discount in risk prior to the election (which is dragging down the overall level of the October future):

With weekly options more popular and liquid than ever, we can see from the chart above that the implied volatility is still highest around the election, but definitely elevated post-election up to inauguration day (except during the week of Christmas, which is typically pretty calm for markets, and, to a lesser extent, during the week of Thanksgiving).

Given these dynamics, an election resolution that is not drawn out could lead to a quick compression in post-election implied volatility.

Effects of the first debate and the president’s COVID-19 illness

There have been several market-moving events in the last week, including the public’s reaction to the first presidential debate, President Trump being diagnosed with COVID-19, and the president tweeting an end to fiscal stimulus negotiations. These events have generally been perceived as negative for the president and positive for former Vice President Biden and the Democrats. Polls and prediction markets have shown Biden widening his lead with a higher probability of a “blue wave” scenario (Democrats regain the White House and both chambers of Congress). A more clear-cut election victory for Biden would mean less uncertainty: less dispute regarding the outcome and a less contentious transfer of power. The reaction from volatility markets was exactly along these lines:

The overall shift downward in the VIX futures curve represents lower expected risk at all horizons, but the decrease was by far the biggest in the November and December contracts. The market reacted to the week’s news by lowering the probability of a chaotic election aftermath, but that is not to say, though, that the market removed that possibility altogether:

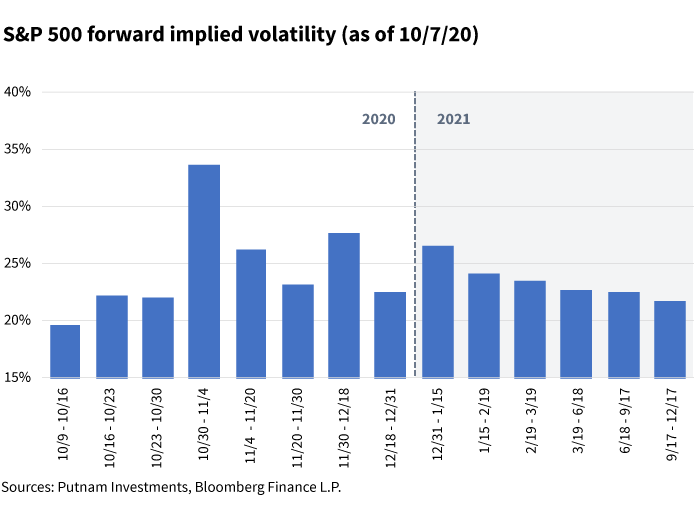

When we view volatility in greater detail, we still see a volatility premium priced in after the election, especially in the first few weeks of December, a period that includes the meeting of the Electoral College on December 14, 2020). When compared to the same data at the end of September, there are still outsized risks around the election and its immediate aftermath, but markets now expect less volatility.

Read more about the Global Asset Allocation Team's current views in Capital Markets Outlook.

323580

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.