The first nine months of 2022 have been challenging. Equity and fixed income markets have both fallen in value by more than 10% through September 30 (as measured by the S&P 500 Index and the Bloomberg U.S. Aggregate Bond Index). For both asset classes to be down by such a large amount at this point of the calendar year is something we’ve never seen before. Within fixed income markets, interest rates have risen dramatically this year, driven by aggressive Federal Reserve tightening aimed at stemming stubbornly high inflation. For context, year to date, the 2-year Treasury yield is 355 bps higher, the 5-year Treasury yield rose 283 bps, and the 10-year Treasury yield climbed 232 bps.

U.S. yield curve change

Source: U.S. Treasury.

The Fed has already hiked the federal funds rate by 300 bps this year and the market is projecting an additional 125 bps of rate increases by year-end. The Fed has also launched quantitative tightening, and up to $95B per month in maturing Treasuries and mortgage-backed securities will not be reinvested. This will further restrict monetary policy as the Fed removes cash from the system. Geopolitical tensions, with the war in Ukraine, have put added pressure on markets in the form of volatile energy prices as well as concern over escalation.

As a result, there has been virtually no place to hide for investors. This environment differs from other periods going back to 1977. The last eight times the S&P 500 finished a year losing ground, bonds finished with positive returns. However, that seems very unlikely as the Bloomberg U.S. Aggregate Bond Index, a widely tracked index, has fallen by more than 10% year to date. In turn, many bond portfolios that are benchmarked to the Aggregate Index have experienced large negative total returns.

Amid widespread negative returns, one area continuing to generate positive total returns is the capital preservation space, including stable value funds. Despite significant market volatility, stable value funds have been doing and are continuing to do exactly what they intend: seek to provide downside risk mitigation and positive absolute returns in various market environments.

An update on market-to-book ratios and crediting rates

The significant sell-off across the Treasury curve in 2022 has caused market-to-book ratios of stable value funds to fall well below 100% for the first time since early 2018. In fact, market-to-book ratios are now at their lowest point since 2008, during the global financial crisis. As of June 30, the average market-to-book ratio of the Morningstar US CIT Stable Value Index stood at 95.32%.

Lower market-to-book ratios may impact how stable value managers utilize the 12-month put option for plan-level withdrawals. Still, these shifting ratios have not had a negative effect on returns so far this year.

Consider the behavior of crediting rates of pooled stable value funds.

The crediting rate formula is designed to smooth the return stream of stable value funds by protecting investors from the quarter-to-quarter principal fluctuations due to changes in the market value of underlying securities. The formula does incorporate any market value gains/losses from the underlying portfolio. However, these gains/losses are amortized into the rate participants receive over the full duration of the portfolio instead of being recognized immediately by changes in the net asset value. Additionally, the formula takes into consideration changes, either higher or lower, in the underlying yields of the fixed income portfolio. Crediting rates on many synthetic contracts reset on a quarterly basis.

Year to date, higher yields have more than offset the amount of market value losses amortized into the crediting rate. As a result, stable value crediting rates have been quite resilient in 2022 and are generally higher compared with where they were at the end of 2021. That said, we would caution that there may be some reversal in crediting rates in the future as any remaining market value losses are amortized over time.

As a reminder, changes to crediting rates of stable value funds are influenced by changes in underlying yields, past and future market value performance, duration positioning, and cash flows in and out of a given fund.

Looking ahead

We believe the probability of withdrawals from a fund is an underappreciated risk that is essential to consider when evaluating stable value funds. Managers that structure their funds to provide ongoing liquidity at par should be in a much better position to deliver consistent returns than those that give minimal consideration to liquidity.

Withdrawal risk is potentially more acute and clearly more detrimental during periods immediately following rising interest rates and/or widening credit spreads. If bonds are sold from wrapped strategies to fund withdrawals at a discount/loss, that loss is embedded in the market-to-book ratio of that strategy, as the securities sold do not have any chance to recover. As mentioned, rising interest rates and volatility throughout 2022 have driven market-to-book ratios lower, which may eventually force some managers to liquidate assets at losses to fund participant activity. This may result in falling crediting rates while interest rates are rising. This directional difference can be quite difficult to explain to plan sponsors and participants and is why it is important to protect underlying strategies from liquidity-driven sales.

In our recent article, "Why withdrawal risk matters in stable value funds," we provide further detail on this potential problem. Stable value funds without adequate liquidity may experience further deterioration in market-to-book ratios if withdrawals occur. This activity may negatively impact the crediting rates of funds that do not have adequate liquidity more than funds better positioned to manage outflows within a short time frame.

This is why we believe that evaluating the structure of a stable value fund is an important component of understanding a manager’s ability to meet outflows without disrupting long-term expected return.

Long-term value proposition remains stable

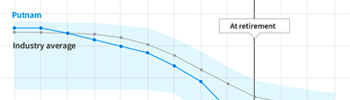

Stable value returns

Sources: Federal Reserve, Morningstar, ICE BofA.

Over the last 30+ years, stable value funds have delivered significantly higher returns than money market funds with less return volatility.

Despite the challenging current market environment, we continue to believe that stable value funds are an attractive capital preservation option for defined contribution plans relative to other options.

For more information about stable value, see "How we invest."

331074

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.